Table of Contents

Introduction:

In today’s financially driven world, having a solid credit score is paramount. Whether you’re looking to secure a mortgage, car loan, or even a credit card with favorable terms, understanding and improving your credit score is crucial. In this comprehensive guide, we’ll delve into the intricacies of discovering and boosting your credit score.

.jpeg "Credit Score Unveiled: 5 Ways On How to Discover and Boost Your Financial Power")

Section 1: What is a Credit Score? A Comprehensive Overview

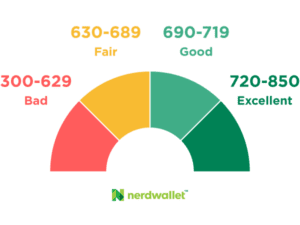

A credit score is a three-digit number, typically ranging from 300 to 850 in the United States, that acts as a snapshot of your financial responsibility and creditworthiness. Lenders use your credit score to assess the risk associated with lending you money or extending credit.

The higher your credit score, the more likely you are to be approved for loans, credit cards, and other financial products, often with lower interest rates and better terms. Conversely, a lower credit score can limit your options and result in higher interest rates, potentially costing you more in the long run.

How Credit Scores Are Calculated: Understanding Your Financial Reputation

Your credit score is a three-digit number that represents your creditworthiness, or how likely you are to repay borrowed money responsibly. It’s a critical factor in determining your eligibility for loans, credit cards, and even certain housing rentals. Understanding how credit scores are calculated can empower you to make informed financial decisions and improve your overall financial health.

The Two Primary Credit Scoring Models

In the United States, two main credit scoring models are used by lenders to assess creditworthiness:

- FICO® Score: This is the most widely recognized and utilized credit scoring model, employed by a vast majority of top lenders. FICO scores range from 300 to 850, with higher scores indicating better creditworthiness. The calculation of a FICO score takes into account five key factors:

- Payment History (35%): Your track record of paying bills on time, including credit cards, loans, utilities, and other debts. Late payments can significantly impact your score.

- Amounts Owed (30%): The total amount of debt you have outstanding, including credit card balances, loan amounts, and other liabilities. Your credit utilization ratio, which is the percentage of your available credit that you’re using, is also considered.

- Length of Credit History (15%): How long you’ve been using credit responsibly. A longer credit history generally reflects greater financial stability and maturity.

- Credit Mix (10%): The diversity of your credit accounts, including credit cards, loans, mortgages, and other types of credit. A healthy mix of credit can demonstrate responsible borrowing behavior.

- New Credit (10%): How often you apply for and open new credit accounts. Multiple credit inquiries in a short period can suggest increased credit risk.

- VantageScore®: This model is gaining traction as an alternative to FICO and is used by some lenders. VantageScore scores also range from 300 to 850, but they may weigh the same factors slightly differently than FICO. The specific algorithms used by both models are proprietary, but understanding the general factors involved can help you manage your credit effectively.

Why Your Credit Score Matters

Your credit score serves as a snapshot of your financial responsibility and is a crucial factor in various financial transactions. A higher credit score can unlock several benefits:

- Lower Interest Rates: Lenders often offer lower interest rates on loans and credit cards to individuals with good credit scores, saving you money over time.

- Better Loan Terms: A good credit score can help you qualify for loans with more favorable terms, such as lower down payments or longer repayment periods.

- Increased Credit Card Rewards: Many credit card issuers offer exclusive rewards and benefits to cardholders with excellent credit scores.

- Easier Approval for Rentals: Landlords and property management companies often check credit scores when evaluating rental applications.

By understanding how credit scores are calculated and the factors that influence them, you can take proactive steps to improve your creditworthiness and enjoy the many benefits of a good credit score. Remember, building good credit takes time and effort, but the rewards are well worth it in the long run.pen_sparktunesharemore_vert

Why Credit Scores Matter:

Your credit score impacts various aspects of your financial life:

- Loan and Credit Card Approvals: Lenders use your score to determine your eligibility and the interest rates you’ll receive.

- Insurance Premiums: In some states, insurers may use credit-based insurance scores to assess risk and set premiums.

- Rental Applications: Landlords often check credit scores to evaluate potential tenants’ financial responsibility.

- Employment: Some employers may check credit reports as part of background checks, particularly for positions with financial responsibilities.

Improving Your Credit Score:

Here are some key steps to build and maintain a good credit score:

- Pay Bills on Time: This is the most crucial factor. Set reminders or automate payments to ensure you never miss a due date.

- Reduce Debt: Pay down outstanding balances to lower your credit utilization ratio.

- Use Credit Responsibly: Avoid maxing out credit cards and only borrow what you can comfortably repay.

- Limit New Credit Applications: Applying for too much credit in a short period can negatively impact your score.

- Monitor Your Credit Report: Regularly check your credit reports for errors and dispute any inaccuracies.

Section 2: How to Discover Your Credit Score

- Free Annual Credit Reports:

Obtain a free credit report annually from each of the three major credit bureaus – Equifax, Experian, and TransUnion. These reports provide a comprehensive overview of your credit history.

- Credit Monitoring Services:

Consider using credit monitoring services that provide real-time updates on your credit score. Many financial institutions and third-party services offer this feature.

- Credit Card Statements:

Some credit card companies now include your credit score on your monthly statements. Check with your issuer to see if this service is available to you.

Section 3: Factors Affecting Your Credit Score

Understanding the components that influence your credit score is essential for improvement:

- Payment History (35%):

Timely payments on bills and credit accounts have the most significant impact on your credit score.

2. Credit Utilization (30%):

The ratio of your current credit card balances to your credit limit affects your score. Aim for a utilization rate below 30%.

- Length of Credit History (15%):

The longer your credit history, the better. Avoid closing old credit accounts, as this can negatively impact this aspect of your score.

- Types of Credit in Use (10%):

A diverse mix of credit types (credit cards, mortgages, installment loans) can positively influence your score.

- New Credit (10%):

Opening several new credit accounts in a short period may be perceived as risky behavior, potentially lowering your score.

Section 4: Tips for Boosting Your Credit Score

- Pay Bills on Time:

Consistently making timely payments is the most effective way to boost your credit score.

- Reduce Credit Card Balances:

Lowering credit card balances helps improve your credit utilization ratio.

- Keep Old Accounts Open:

Closing old credit accounts can shorten your credit history, potentially lowering your score. Keep them open and occasionally use them to maintain activity.

- Monitor Your Credit Report:

Regularly check your credit report for errors or fraudulent activity. Dispute any discrepancies promptly.

- Diversify Your Credit Mix:

Consider diversifying your credit portfolio by adding different types of credit, such as an installment loan.

Conclusion:

Discovering and optimizing your credit score is a journey that requires diligence and patience. By understanding the key factors influencing your score and implementing strategic actions, you can take control of your financial future. Regular monitoring and responsible financial habits are the keys to unlocking a higher credit score and better financial opportunities. Start your journey today and pave the way for a brighter financial tomorrow.